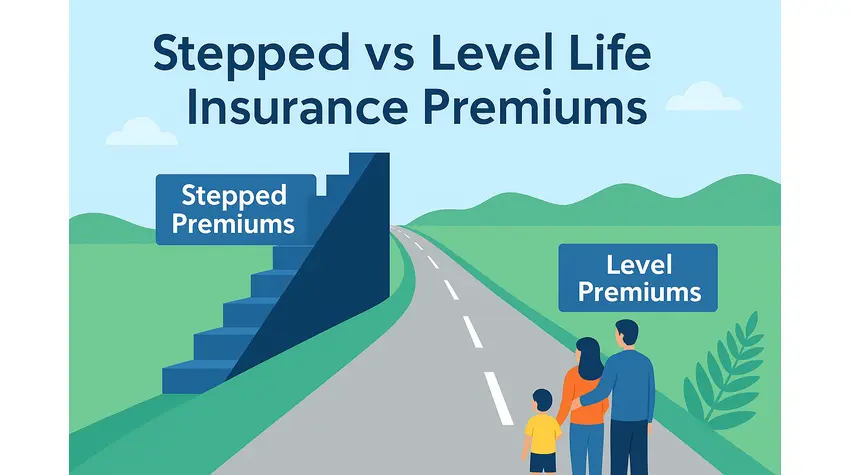

Life Insurance Myths in New Zealand

Life insurance is one of the most essential financial tools for securing your family’s future, yet many Kiwis misunderstand how it works. Myths and misconceptions often prevent people from getting the right coverage—or any coverage at all.

Some believe life insurance is only for the elderly, while others assume it’s too expensive or that insurers never pay. These misconceptions can lead to poor financial decisions, leaving families vulnerable in times of crisis.

The truth? Life insurance is more accessible, affordable, and beneficial than you might think.

In this guide, we’ll debunk the most common life insurance myths in New Zealand, helping you make informed decisions about protecting your family. Let’s separate fact from fiction! ✅

Category 1: Misconceptions About Who Needs Life Insurance

Myth 1: Life Insurance is Only for Older People

Many Kiwis believe that only retirees or the elderly need life insurance.

The Truth:

✔️ Younger people get lower premiums – The younger and healthier you are, the cheaper your policy.

✔️ Life insurance isn’t just for death benefits—many policies offer living benefits, like income protection or trauma insurance.

✔️ Future-proof your finances – Secure your financial future – Getting covered early ensures protection before health conditions arise

💡 Example: A 25-year-old non-smoker can lock in a $500,000 policy for $25/month, while a 50-year-old would pay $100+ for the same coverage.

Myth 2: My Employer’s Life Insurance Is Enough

The Misconception:

Many Kiwis assume that their employer’s life insurance is sufficient to cover their family’s needs.

The Truth:

✔️ Employer-provided life insurance is limited—it typically covers only 1 to 2 times your annual salary, which may not be enough to support your family long-term.

✔️ If you change jobs, retire, or get laid off, you usually lose your coverage.

✔️ Employer policies don’t cover critical illness, trauma insurance, or personal customisation.

💡 Real-Life Scenario:

📌 David, a 38-year-old IT professional, relied on his employer’s 1x salary life insurance policy. When he lost his job, he also lost his coverage. When he tried to purchase private life insurance, he was diagnosed with high blood pressure, which increased his premiums by 40%. Had he secured a personal policy earlier, he could have locked in lower rates for life.

📊 Statistical Insight:

🔹 A 2022 Financial Services Council NZ survey found that 53% of Kiwis wrongly believe employer life insurance is sufficient, while only 25% of employer policies exceed $100,000 coverage—far below what most families need.

📌 Takeaway:

Your employer’s policy is not permanent or sufficient—get personal coverage for complete protection.

Myth 3: Life Insurance is Only for People with Kids

Many Kiwis believe life insurance is essential for parents with children who rely on their income. The common assumption is that you don’t need financial protection if you don’t have dependents.

The Truth:

This is one of the biggest misconceptions about life insurance. While having children is a strong reason to get covered, life insurance offers far more benefits than protecting kids. It can provide financial security to partners, businesses, and family members or even cover personal debts.

Here’s why life insurance can still be crucial—even if you don’t have children:

✔️ It protects your partner or spouse – If your partner relies on your income, life insurance ensures they can maintain their standard of living without financial strain. Even if they work, losing a significant income could mean downsizing or struggling with bills.

✔️ It secures your business – If you’re self-employed or own a business, life insurance can help cover outstanding business debts, employee wages, and operational expenses, preventing your business from collapsing if something happens to you.

✔️ It helps cover outstanding debts – If you have a mortgage, student loan, or personal debt, they don’t disappear when you pass away. Your family or estate may still be responsible for them. Life insurance ensures those debts are paid off so they aren’t passed on to loved ones.

✔️ It pays for your funeral expenses – The average funeral in New Zealand can cost anywhere from $10,000 to $15,000. A life insurance payout can cover these costs, preventing financial stress on your family.

✔️ It provides long-term financial security – Certain life insurance policies offer investment options, allowing you to build cash value over time—benefiting wealth planning, estate transfers, and retirement security

💡 Example: Olivia, a 29-year-old business owner in Wellington, took out a life insurance policy to cover her business loans. She didn’t have kids yet, but she wanted to ensure that if something happened to her, her business partner wouldn’t be left with the financial burden of repaying company debts. Her policy also included a small lump sum payout for her partner to manage living costs in the short term.

📌 Looking for the right life insurance policy? Compare policies instantly with Compare Life Cover and find the best option!

Myth 4: ACC Provides Comprehensive Coverage

The Misconception:

Many Kiwis believe that ACC (Accident Compensation Corporation) covers all medical expenses and lost income, so they don’t need life or income protection insurance.

The Truth:

✔️ ACC only covers injuries caused by accidents—not illnesses, long-term disabilities, or natural causes.

✔️ If you are diagnosed with cancer, stroke, heart disease, or any chronic illness, ACC will not cover your lost wages.

✔️ ACC pays only a portion of your income—up to 80% of lost earnings, but with strict eligibility requirements.

💡 Real-Life Scenario:

📌 Daniel, a 42-year-old self-employed builder, suffered a heart attack and was unable to work for eight months. Since his condition was not accident-related, ACC provided no income support. Luckily, Daniel had income protection insurance, which covered 75% of his income while he recovered. Without it, his mortgage and household expenses would have been impossible to manage.

📊 Statistical Insight:

🔹 A 2023 Financial Services Council NZ survey found that 40% of New Zealanders mistakenly believe ACC covers all health-related income loss, leading many to forego critical life and income protection insurance.

📌 Takeaway:

Don’t assume ACC will cover all risks—consider income protection insurance to safeguard against unexpected health conditions.

Myth 5: Life Insurance Payouts Are Taxed in New Zealand

A common misconception is that life insurance payouts are subject to income tax in New Zealand, meaning beneficiaries would receive less than the full policy amount.

The Truth:

✔️ No Income Tax on Payouts – Life insurance death benefits in New Zealand are not subject to income tax, meaning your beneficiaries receive the full payout.

✔️ No GST on Premiums—Unlike some other financial products, life insurance premiums are not subject to the Goods and Services Tax (GST) in New Zealand.

✔️ Business-Owned Policies May Differ – Business-owned life insurance policies, such as key person insurance, may have different tax rules. Always check with a financial advisor for business-related coverage.”

💡 Example: Anna, a Wellington resident, left her son a $500,000 life insurance policy. He received the full amount tax-free, which helped him cover the mortgage and living expenses.

Myth 6: Only the Working Parent Needs Life Insurance

Many believe only the parent bringing in an income needs life insurance, assuming that a stay-at-home parent doesn’t contribute financially. However, this misconception overlooks the immense financial value a stay-at-home parent provides in daily household management, childcare, and support.

The Truth:

A stay-at-home parent may not receive a paycheck, but their contributions to the household are essential and costly to replace. If they were to pass away unexpectedly, the financial strain on the surviving partner could be significant. Here’s why both parents need life insurance:

✔️ A stay-at-home parent provides financial value – A stay-at-home parent provides essential services—childcare, cooking, cleaning, transportation, and home management—that would be costly to outsource. The estimated cost of replacing these services in New Zealand could exceed $40,000 annually.

✔️ The surviving parent may need to reduce work hours – If a stay-at-home parent passes away, the working parent may have to take unpaid leave, reduce work hours, or find alternative childcare arrangements, which impact income and stability. A life insurance payout can ease this financial burden.

✔️ Childcare costs are significant – Daycare or hiring a nanny can cost $250-$400 per week per child in New Zealand. Life insurance can ensure continuity of care for children without financial strain.

💡 Example: Sarah, a stay-at-home mom to two children, passed away unexpectedly. Her life insurance policy provided her husband with a lump-sum payout, which helped him afford childcare and household support while he continued working. Without it, he would have faced the difficult choice of reducing work hours or struggling with financial and caregiving responsibilities alone.

Category 2: Myths About When & Why to Buy Life Insurance

Myth 7: I’m Too Young to Get Life Insurance

Many young people believe that life insurance is something they can worry about later in life—perhaps when they have children, a mortgage, or are older. However, waiting to get life insurance can be a costly mistake. The reality is that buying life insurance early provides significant financial advantages, including lower premiums and guaranteed coverage.

The Truth:

✔️ Premiums Are Much Cheaper When You’re Young – Life insurance premiums are calculated based on age, health, and risk factors. A younger, healthier person pays significantly less than an older applicant. By locking in a policy early, you secure lower rates for the long term, saving thousands over time.

✔️ Delaying Could Lead to Higher Premiums or Coverage Denials – If you wait too long, health conditions such as high blood pressure, diabetes, or other chronic illnesses may develop. Insurers may charge much higher premiums or, in some cases, deny coverage altogether if health risks increase.

🔹 Example: At 26, Emma was in excellent health and assumed she didn’t need life insurance. By 34, she was diagnosed with Type 2 diabetes, which increased her life insurance premium by 60%. Had she purchased a policy earlier, she could have locked in a lower rate for life.

✔️ Even Without Dependents, Life Insurance Protects Your Future – While you may not have a family or mortgage yet, your future financial responsibilities will grow. Life insurance can help:

-

- Cover personal debts (e.g., student loans, credit cards).

- Secure lower rates when you have dependents.

- Provide financial security if you’re self-employed or running a business.

Myth 8: My Health Will Prevent Me from Getting Covered

Coverage Options for High-Risk Individuals

The Truth:

Many Kiwis think a pre-existing condition means automatic rejection. That’s not true!

💡 Many insurers offer coverage even with pre-existing conditions—while your health may affect the cost, it doesn’t mean automatic rejection.”

Here’s what you can do:

✔️ Look for specialised high-risk policies.

✔️ Consider Medical insurance if your health affects your ability to work.

✔️ Compare providers that offer life insurance for high-risk individuals.

📌 Pro Tip: Some insurers charge extra for high-risk applicants, but others provide competitive rates—always compare policies!

Myth 9: I Don’t Need Life Insurance Because I Have Savings

People assume their savings will be enough to protect their loved ones.

The Truth:

✔️ The average funeral in NZ costs $10,000+, which can drain savings fast.

✔️ A sudden illness or accident can wipe out years of savings.

✔️ A $500,000 life insurance policy offers more protection than most savings accounts.

💡 Example: James, 40, had $50,000 saved, but his mortgage was $350,000. His life insurance payout ensured his family could stay in their home.

Myth 10: Life Insurance is Too Expensive

Many Kiwis avoid life insurance because they believe it’s too costly or only for wealthy individuals. However, life insurance is often more affordable than people think—especially if you compare policies and take advantage of available discounts. A basic life insurance policy can cost less than a daily cup of coffee ☕.

The Truth:

✔️ Customisable Coverage – Many life insurance providers allow you to adjust your coverage amount, payment frequency, and optional benefits to fit your budget.

✔️ Discounts Are Available – Insurers offer lower premiums for non-smokers, people in good health, or those who bundle policies like income protection or trauma insurance.

✔️ Comparing Saves Money – Different insurers offer different pricing. Shopping around ensures you get the best coverage at the lowest cost.

✔️ Small Payments, Big Protection – A basic policy can provide financial security for your family without costing a monthly fortune.

🔹 Example: Mike, 28, used a life insurance comparison tool and found that one insurer charged $45/month while another offered the same coverage for $30/month. By taking five minutes to compare, he saved $180 per year on his policy.

📌 Want to see how much you could save? Compare life insurance quotes today with Compare Life Cover

Category 3: Myths About How Life Insurance Works

Myth 11: Life Insurance Only Pays Out When You Die

Some think life insurance only benefits their loved ones after they pass away.

The Truth:

✔️ Living benefits exist! Some policies pay out while you’re alive.

✔️ Trauma insurance provides a lump sum if you’re diagnosed with a critical illness.

✔️ Income protection insurance replaces lost income if you can’t work.

💡 Example: Emma suffered a stroke but had trauma insurance. She received a $200,000 payout to cover medical bills and home adjustments.

Myth 12: Insurance Providers Won’t Pay Out Anyway

Some believe insurers always find ways to deny claims.

The Truth:

✔️ 98% of life insurance claims in NZ are paid out.

✔️ Denials only happen due to non-disclosure, policy exclusions, or unpaid premiums.

✔️ Reading the fine print and disclosing medical history prevents issues.

Example: Rachel’s Story: Rachel’s husband had a $750,000 life insurance policy but didn’t disclose a pre-existing condition when applying. When he passed away, his claim was denied due to non-disclosure. Had he been honest about his health, he could have secured a policy with slightly higher premiums—but full coverage.

📊 Statistical Insight:

🔹 98% of claims are approved in New Zealand, but 20% of denials are due to non-disclosure—proving that being transparent on applications is key.

Myth 13: Medical Exams Are Mandatory and Invasive

Some people avoid applying for life insurance because they fear medical exams.

The Truth:

✔️ Many policies offer instant online approval with no medical exams required.

✔️ Some insurers base premiums on self-reported health information.

✔️ Guaranteed acceptance policies exist for people with medical conditions.

Myth 14: Life Insurance is Complicated and Confusing

Many believe life insurance is too complex, with confusing terms, hidden clauses, and overwhelming options. As a result, they avoid getting covered—thinking they won’t understand the policy or that it requires too much effort. However, modern tools and expert guidance have made buying life insurance more effortless than ever.

The Truth:

✔️ Online Comparison Tools Simplify Everything – No more calling multiple insurers or reading endless brochures. With life insurance comparison tools, you can see quotes side by side, compare coverage, and choose the best option in minutes.

🔹 Example: James, a 35-year-old Wellington resident, thought finding life insurance was too hard. However, after using an online tool, he compared three top insurers in under five minutes and found an affordable policy without stress.

✔️ Customisable & Flexible Policies Exist – Many insurers tailor policies to match your lifestyle, budget, and coverage needs. Whether you need income insurance, trauma insurance or additional riders, flexible solutions are designed to fit your situation.

📌 Want an easy way to find the best policy? Compare Life Cover helps Kiwis quickly find clear, transparent policies that are free of confusion. Get started today!

Conclusion

🚀 Life insurance isn’t as complicated or expensive as people think! Understanding the truth behind these myths allows you to make smarter choices and secure your financial future.

📌 Next Step: Compare policies with Compare Life Cover and find the right insurance for your needs today!

{kind=link}

{kind=link}

{kind=link}

{kind=link}